Chancellor Rachel Reeves has unveiled a hopeful economic outlook in her recent spring statement, asserting that households can expect to be better off by over £1,000 annually by the next general election. However, the ongoing turmoil in the Middle East has cast a shadow over these optimistic forecasts, raising concerns about inflation and household finances as energy prices surge.

Promises of Improved Household Finances

In her spring statement, Reeves expressed confidence in the government’s economic policies, claiming they are set to deliver tangible benefits to households suffering from the effects of the cost of living crisis. The Chancellor’s key pledge is that by the next general election, the average household will see an increase in disposable income, rising from £25,600 to an estimated £26,685—a difference of approximately £1,085.

This figure represents “real household disposable income,” which accounts for taxes and inflation. The Office for Budget Responsibility (OBR) has projected a modest annual growth of 0.6% to 0.9% in disposable income from 2026 to 2030. However, this forecast may be tempered by the government’s decision to freeze income tax thresholds until 2031, which could lead to more individuals being pushed into higher tax brackets as they receive pay increases—an effect known as fiscal drag.

Inflation and Energy Costs on the Rise

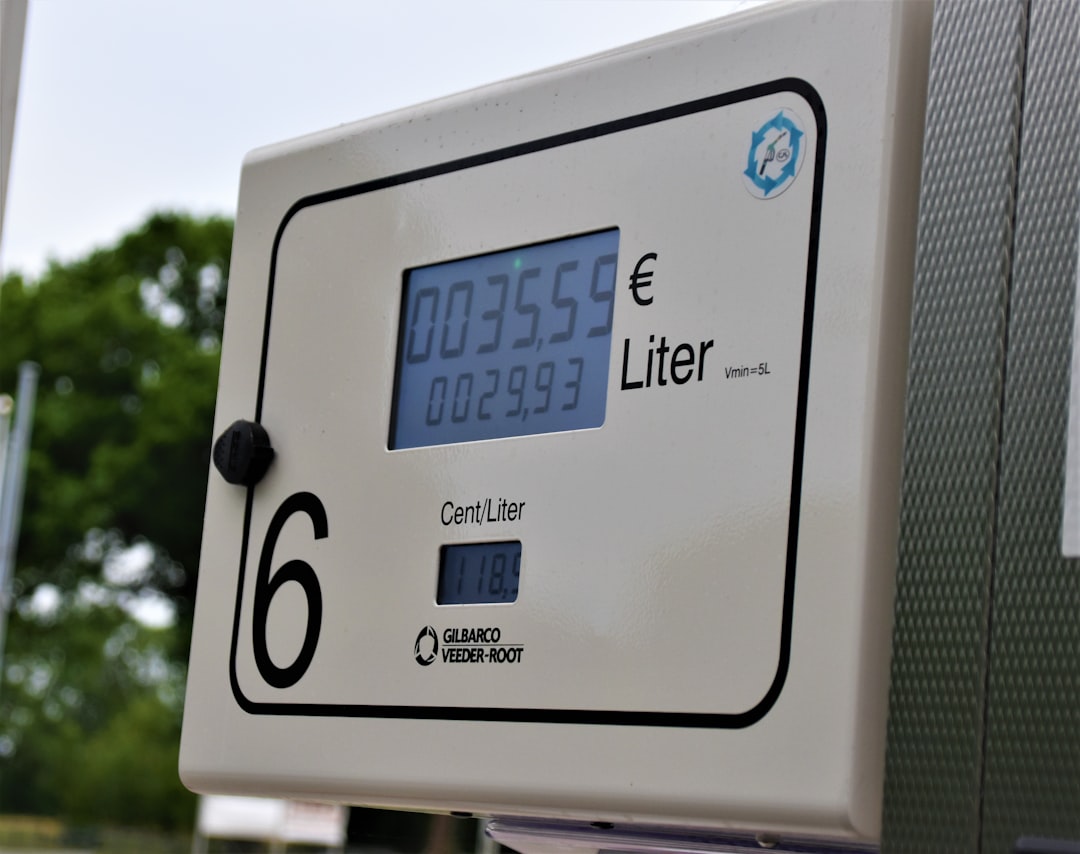

While the OBR anticipates that inflation will stabilise at or near the 2% target over the next five years, recent geopolitical events have raised fresh concerns. The crisis in Iran has led to a surge in energy prices, prompting fears of renewed inflationary pressures. Just as the nation began to see some relief from the cost of living crisis, the prospect of rising energy bills looms large.

The government has already committed to reducing average household energy bills by £150 this year, and the energy regulator Ofgem has announced a 7% decrease in its price cap, bringing it down to £1,641 for typical dual-fuel households. However, analysts are warning that sustained increases in wholesale gas prices could push the price cap back up to nearly £2,500 by July, depending on how long the current volatility persists.

Mortgage Rates and Housing Market Outlook

In terms of housing costs, Reeves noted that recent interest rate cuts have allowed homeowners to save significantly on mortgage repayments. For example, someone taking out a two-year fixed mortgage can now save over £1,300 annually compared to previous rates. The average rate on a two-year fixed mortgage has decreased to 4.83%, down from over 5% a year ago.

However, the ongoing Middle East conflict has cast uncertainty over future interest rates. While the Bank of England has cut rates several times since the last general election, market predictions for further cuts have diminished, with the likelihood of a reduction in March now estimated at about 30%. This uncertainty could lead to fluctuations in mortgage rates, which the OBR expects to rise gradually over the next few years.

Employment and Economic Growth Concerns

The OBR has also revised its economic growth forecast downwards, now predicting a growth rate of just 1.1% for the year, compared to an earlier estimate of 1.4%. Unemployment rates, which are already at a five-year high, are expected to rise further to 5.3% as job seekers struggle to find opportunities amidst weak hiring demand.

Experts have expressed concern about the implications of rising oil prices on inflation and the broader economy. Dan Coatsworth from AJ Bell remarked that while there may be hope for improved growth in the coming years, the current economic climate remains challenging for both businesses and consumers.

Why it Matters

The unfolding situation in the Middle East poses significant risks to the UK’s economic recovery, particularly in terms of inflation and household budgets. As families face the prospect of rising energy bills and stagnant wages, the government’s optimistic forecasts will be put to the test. The ability of the Treasury to navigate these turbulent waters will be crucial in determining whether households can truly expect a brighter financial future or if they will continue to grapple with the pressures of escalating costs.