The ongoing conflict in Iran is poised to exert the most significant economic pressure on the UK compared to other major economies, according to the Organisation for Economic Co-operation and Development (OECD). The forecast for UK growth in 2023 has been revised downwards to a mere 0.7%, a notable decrease from the earlier estimate of 1.2%. This downturn is compounded by expectations of heightened inflation, signalling a challenging economic environment ahead.

Global Economic Landscape Affected by Conflict

The OECD’s recent assessment highlights a broad downgrade in growth projections across many advanced economies due to the instability arising from the US-Israel conflict with Iran. The potential for a protracted war has raised alarms about “significant energy shortages” on a global scale. The situation is exacerbated by escalating costs of fertilisers, which, if sustained, could severely impact agricultural yields and drive food prices up in the coming year.

The surge in wholesale oil and gas prices, triggered by supply disruptions from the Strait of Hormuz—a critical artery for global oil transport—has already begun to manifest in rising costs for consumers. Drivers in the UK are experiencing increases in petrol and diesel prices, while those reliant on heating oil feel the pinch as well. Furthermore, mortgage lenders have responded by tightening their offers and increasing rates, a move that could further dampen economic activity.

Revised Economic Forecasts

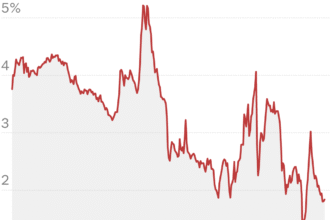

While the OECD maintains its global growth forecast at 2.9% for 2023, it has significantly raised its inflation predictions for G20 nations to an average of 4%, up from 2.8%. For the UK, inflation is now expected to hit 4% this year, a substantial increase from the previous estimate of 2.5%. Notably, only the United States is projected to experience higher inflation rates among G7 nations, while the UK is anticipated to lag behind only Italy in terms of economic growth.

In March, the Office for Budget Responsibility (OBR) had already adjusted its growth forecast for the UK from 1.4% to 1.1%, prior to the escalation of tensions in Iran. The OBR indicated that the conflict could have “very significant” implications for economic conditions.

Political Reactions and Future Outlook

Chancellor Rachel Reeves acknowledged the potential ramifications of the Iran war on the UK economy but maintained confidence in the government’s economic strategy. “The decisions we have taken have put us in a better position to protect the country’s finances and family finances from global instability,” she stated. However, the shadow chancellor, Sir Mel Stride, condemned the downgraded forecasts as a “damning verdict” on the Labour government’s economic management.

The Liberal Democrats have labeled this forecast as a critical alert regarding the government’s purportedly anti-growth policies. The party asserts that the current trajectory is costing families dearly, further intensifying calls for a reevaluation of economic strategies.

Policy Recommendations and Business Concerns

The OECD’s outlook underscores the importance of government interventions to mitigate the impact of soaring energy prices. It stresses that any support measures should be timely, targeted at vulnerable households and viable businesses, while preserving incentives for energy conservation and having clear expiry mechanisms.

In light of the current situation, Reeves has indicated that the government is prepared to assist those most affected by rising energy costs, although any such measures will have to align with fiscal prudence to keep inflation and interest rates manageable.

Concerns from the business sector are mounting, with Stuart Machin, chief executive of M&S, highlighting that “policy costs” related to energy have dramatically increased and are becoming untenable for businesses. Similarly, UK retailer Next has warned of potential additional costs amounting to £15 million if the conflict persists, although it remains hopeful that savings could mitigate some of these impacts.

Why it Matters

The economic forecast from the OECD serves as a stark reminder of how international conflicts can ripple through national economies, particularly in an interconnected world. As the UK grapples with these new economic realities, the government’s ability to navigate rising inflation and stunted growth will be crucial in maintaining public confidence and economic stability. The situation calls for urgent policy responses that not only address immediate concerns but also lay the groundwork for long-term resilience against future global disruptions.